- The 1095-C will be used by ALEs for all full-time employees and can be used for any non-fulltime employee covered by an ALEs self-funded plan.

- The 1095-B will be used by small (non-ALE) employers who sponsor self-funded plans, and can optionally be used by ALEs to report for non-employees (such as retirees, COBRA participants, non-employee board members, etc.) covered by the employer's self-funded plan.

- ALEs will be using the 1095-C for most reporting purposes, so this guide will focus on the 1095-C requirements. ALEs who offer self-funded coverage to non-employees (who choose to optionally use the 1 095-B) and small employers with self-funded plans should refer to IRS 1095-B instructions.

- The Form 1095-C contains three parts, but not all employers must complete all three parts. The specific information required depends on whether the plan is fully-insured or self-funded.

Section 1 - Understanding the 1095

1095 Overview

Employers must provide a Form 1095 (or alternative statement if applicable-see details below) to any employee who was employed full-time for any month during the calendar year. A 1095 must also be provided to any individual (including non-employees) who participated in a self-funded employer sponsored plan during the year.

What is 1095-C?

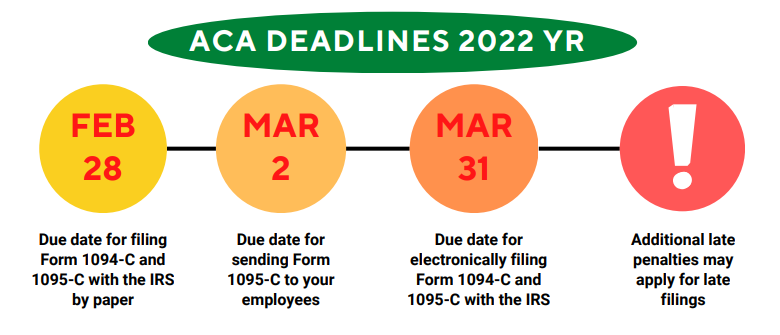

Form 1095-C is filed and furnished to any employee of an Applicable Large Employers (ALE) member who is a fulltime employee for 1 or more months of the calendar. All ALEs must report information for all 12 months of the calendar year for each employee. Penalties for not Filing or Incorrectly Filing Forms 1094/1095-C is $280 per return, up to $3.426 million per business.

Form 1095-C Parts

- Part I - Basic employee and employer information including names, taxpayer ID numbers, address, contact information, etc.

- Part II - Used to report offers of coverage, employee contribution requirements, and employer safe harbors (applicable to that employee), for each month of the calendar year.

- Part III - Used to provide monthly details on covered individuals (including spouses and dependents) covered by the plan during the calendar year. Data includes name, SSN (or DaB if SSN is not available), and an indication of the calendar months for which the individual was covered by the plan.

Which parts of the 1095-C do employers have to complete?

- Applicable Large Employers (ALEs) who sponsor fully-insured plans must complete Parts I and II of the Form 1095-C, but are not required to complete Part III (which details the coverage provided on a monthly basis).

- The carrier providing this fully insured coverage will report to the IRS and issue a 1095 to covered individuals containing the coverage-related information.

- Applicable Large Employers (ALEs) who sponsor self-funded plans must complete all three parts (I, II, and III) of the 109S-C.

- Applicable Large Employers (ALEs) who sponsor both fully-insured and self-funded plans are required to fill out Parts I & II for all full-time employees, and to complete Part III only for individuals who are covered by a self-funded plan.

Our Services

Online Filing We utilize highly rated filing applications to minimize error and direct upload to IRS portal

Hassle Free Simply provide us with an insurance census and we will take care of the rest